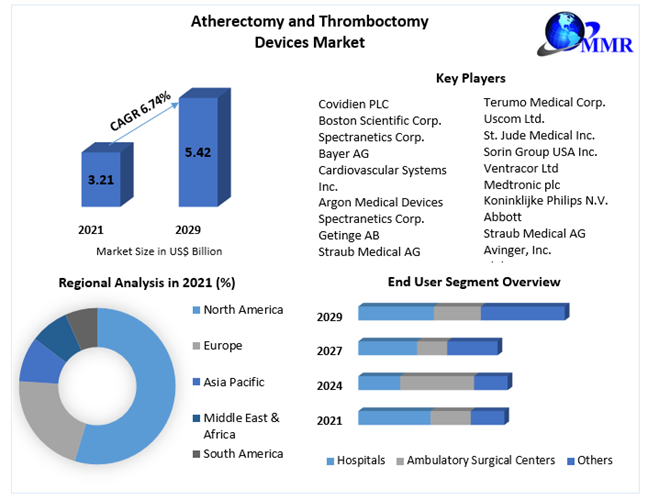

Atherectomy and Thrombectomy Devices Market Projected to Reach USD 5.42 Billion by 2029

The global atherectomy and thrombectomy devices market is expected to reach USD 5.42 billion by 2029, growing at a compound annual growth rate (CAGR) of 6.74%. The market’s growth is driven by technological innovations, increased demand for minimally invasive procedures, and a rising prevalence of vascular diseases.

Market Definition and Scope

Atherectomy devices are medical instruments used to cut and remove atherosclerotic plaque from blood vessels or break down the material into smaller particles for easier removal. These devices play a vital role in the treatment of peripheral and coronary artery disease.

Ask For Sample copy of this report @

Market Growth Drivers and Opportunities

• Technological Advancements: Continuous R&D in device design and imaging technologies is enhancing the accuracy, safety, and effectiveness of atherectomy and thrombectomy procedures.

• Rising Prevalence of Arterial Diseases: The growing incidence of peripheral artery disease and deep vein thrombosis is driving demand for advanced surgical devices that can ensure effective treatment with minimal complications.

• Minimally Invasive Procedures: An increasing number of patients and healthcare providers are opting for less invasive interventions that offer quicker recovery times and reduced hospital stays.

Segmentation Analysis

• By Product Type:

o Rotational Atherectomy Devices

o Excisional Atherectomy Devices

o Directional Atherectomy Devices

o Excimer Laser Atherectomy Devices

o Jetstream Systems

o Orbital Atherectomy Devices

Rotational and laser-based atherectomy systems are gaining popularity due to their efficiency in complex lesion removal and lower rates of complications.

• By End-User:

o Hospitals

o Ambulatory Surgical Centers (ASCs)

o Specialty Clinics and Others

Hospitals currently dominate the end-user segment owing to high patient volumes and access to sophisticated vascular surgery infrastructure. However, ASCs are emerging as a strong growth area due to their efficiency and reduced procedural costs.

Regional Insights

• North America: This region holds a dominant market share, thanks to the strong presence of top medical device manufacturers, high adoption of advanced technologies, and well-established healthcare systems.

• Asia-Pacific: Expected to experience the fastest growth during the forecast period. Countries like India, China, and Japan are seeing increased investments in healthcare infrastructure and a growing awareness of peripheral and coronary artery disease management.

• Europe: Countries such as Germany, France, and the UK contribute significantly due to aging populations and the widespread adoption of vascular intervention techniques.

Competitive Landscape

The global atherectomy and thrombectomy devices market is competitive, with major players focusing on innovation, product launches, and strategic partnerships to gain market share. Key companies operating in this space include:

•

• Spectranetics Corporation

• Terumo Medical Corporation

• Getinge AB

• Argon Medical Devices

• Straub Medical AG

• Vascular Solutions Inc.

• Zoll Medical Corporation

• Uscom Ltd.

• St. Jude Medical Inc.

• Sorin Group USA Inc.

• Ventracor Ltd.

These companies are focused on expanding their portfolios through advanced technologies such as drug-coated systems, laser-assisted therapies, and AI-enabled guidance systems to improve clinical outcomes.

Conclusion

The global atherectomy and thrombectomy devices market is poised for sustained growth in the coming years. Rising demand for minimally invasive solutions, expanding elderly populations, and the rapid pace of technological advancements are expected to reshape the landscape of vascular intervention.

Invisible Orthodontics Market Projected to Reach USD 33.9 Billion by 2030

The global invisible orthodontics market, valued at USD 6.1 billion in 2023, is anticipated to grow at a compound annual growth rate (CAGR) of 28.5%, reaching approximately USD 33.9 billion by 2030.

Market Definition and Estimation

Invisible orthodontics encompasses dental devices such as clear aligners, ceramic braces, lingual braces, and clear retainers designed to straighten teeth and correct misaligned bites discreetly. These alternatives to traditional metal braces offer aesthetic appeal and comfort, making them popular among adolescents and adults seeking orthodontic treatment.

Ask For Sample copy of this report

Market Growth Drivers and Opportunities

Several factors are driving the expansion of the invisible orthodontics market:

1. Increasing Prevalence of Malocclusion: Malocclusion, a misalignment of teeth, is one of the most prevalent dental conditions worldwide, affecting a significant portion of children and adolescents. This high prevalence underscores the growing need for effective orthodontic treatments.

2. Rising Demand for Aesthetic Dental Solutions: The global emphasis on aesthetics has boosted the demand for orthodontic treatments that are both effective and visually discreet. Invisible orthodontic solutions cater to this demand by offering less noticeable treatment options.

3. Technological Advancements: Innovations in dental technology, such as the integration of CAD/CAM systems and 3D printing, have enhanced the customization and efficiency of invisible orthodontic devices, leading to increased adoption among dental professionals and patients.

4. Growing Adult Patient Population: There is a notable increase in adults seeking orthodontic treatment, driven by the desire for improved dental aesthetics and function. Invisible orthodontics provides a suitable solution for this demographic, contributing to market growth.

Segmentation Analysis

The invisible orthodontics market is segmented based on product type, age group, application, end-user, and distribution channel.

• By Product Type:

o Clear Aligners

o Ceramic Braces

o Lingual Braces

o Clear Retainers

• By Age Group:

o Children

o Teenagers

o Adults

• By Application:

o Malocclusion

o Crowding

o Excessive Spacing

o Others

• By End-User:

o Hospitals

o Dental Clinics

o Orthodontic Clinics

o Others

• By Distribution Channel:

o Direct Sales

o Third-Party Distributors

Regional Insights

• North America: Dominated the market in recent years, attributed to advanced healthcare infrastructure, high awareness of dental aesthetics, and the presence of key market players.

• Asia-Pacific: Expected to register the fastest growth during the forecast period, driven by increasing disposable incomes, growing awareness of orthodontic treatments, and expanding healthcare infrastructure.

Competitive Analysis

The invisible orthodontics market features several key players dedicated to advancing dental solutions:

• Align Technology, Inc.: Renowned for its Invisalign system, offering clear aligner treatments worldwide.

• 3M Company: Provides a comprehensive range of orthodontic products, including ceramic and lingual braces.

• Dentsply Sirona: Offers innovative dental solutions, including clear aligners and other orthodontic products.

solutions.

Conclusion

The invisible orthodontics market is set for significant growth, driven by the increasing prevalence of dental malocclusions, rising demand for aesthetic dental treatments, technological advancements, and a growing adult patient population. Addressing challenges such as high treatment costs and enhancing awareness about available orthodontic options will be crucial for sustaining this growth trajectory.

Pharmaceutical Contract Sales Outsourcing (CSO) Market Poised for Significant Growth

Pune, Maharashtra, India – March 26, 2025 – The global Pharmaceutical Contract Sales Outsourcing (CSO) market is projected to experience substantial growth, with expectations to reach USD 19.14 billion by 2030, advancing at a compound annual growth rate (CAGR) of 7.2% during the forecast period. This surge is driven by the evolving dynamics of the pharmaceutical industry and the increasing trend of companies outsourcing their sales and marketing operations to specialized contract sales organizations

Market Potential & Opportunities

The pharmaceutical sector has witnessed dynamic expansion, propelled by heightened global healthcare expenditures and the escalating demand for novel drugs addressing unmet clinical needs. To navigate the complexities of market expansion and regulatory compliance, numerous small and medium-sized pharmaceutical companies are turning to CSOs for their sales and marketing functions. This strategic move enables these companies to focus on core competencies such as research and development, while leveraging the expertise of CSOs to enhance market penetration and operational efficiency.

Request for sample data report @

Segmentation Analysis

The Pharmaceutical CSO market is segmented based on sales type and service type. The dedicated sales model emerges as the predominant approach, wherein a specialized team is exclusively assigned to a client's project. This model ensures focused attention and alignment with the client's objectives, facilitating effective market strategies and execution.

Regional Insights

North America and Europe are anticipated to maintain a dominant position in the CSO market, collectively accounting for approximately 70-75% of global revenues. This dominance is attributed to stringent regulatory frameworks and a well-established culture of outsourcing within these regions. Conversely, the Asia Pacific market is projected to exhibit rapid growth, fueled by increasing disposable incomes, a large patient population, and proactive government initiatives aimed at enhancing healthcare infrastructure

Key Players

The market landscape features a mix of established entities and emerging players, all contributing to the competitive environment. While the report profiles fifteen key players from various regions, it acknowledges the broader spectrum of market leaders, followers, and new entrants, each playing a pivotal role in shaping the industry's trajectory.

Conclusion

The Pharmaceutical Contract Sales Outsourcing market is on an upward trajectory, driven by the need for pharmaceutical companies to optimize operations and extend their market reach. By partnering with CSOs, these companies can navigate the complexities of the industry more effectively, ensuring compliance and enhancing profitability. As the market continues to evolve, stakeholders are encouraged to stay abreast of trends and leverage opportunities to maintain a competitive edge.

About Maximize Market Research

Maximize Market Research is a global market research and business consulting firm, providing clients with data-driven insights and strategic guidance across various industries. With a team of experienced professionals, the company delivers comprehensive reports and analyses to support informed decision-making.

Retinal Vein Occlusion Market Poised for Significant Growth Through 2029

Pune, India – March 26, 2025 – The global Retinal Vein Occlusion (RVO) market, valued at USD 13.90 billion in 2022, is projected to experience a robust compound annual growth rate (CAGR) of 10.7%, reaching approximately USD 28.33 billion by 2029. This substantial growth is driven by the increasing prevalence of vascular and ophthalmic disorders, advancements in treatment technologies, and heightened investments in research and development

Request for sample data report @

Market Potential & Opportunities

The escalating incidence of conditions such as lymphoma, glaucoma, myeloma, atherosclerosis, and diabetes has significantly contributed to the rising cases of RVO globally. Lifestyle changes and an aging population further exacerbate the prevalence of eye diseases, underscoring the urgent need for effective treatment solutions. Technological innovations, particularly in anti-vascular endothelial growth factor (anti-VEGF) therapies and laser treatments, have revolutionized RVO management, offering promising avenues for market expansion. Additionally, increased investments by key industry players in product development and portfolio diversification are expected to propel market growth in the coming years.

Segmentation Analysis

The RVO market is segmented based on type into Central Retinal Vein Occlusion (CRVO) and Branch Retinal Vein Occlusion (BRVO). In 2022, the CRVO segment dominated the market and is anticipated to maintain its leading position throughout the forecast period. This dominance is attributed to the concerted efforts of major pharmaceutical companies in developing targeted therapeutics for CRVO, coupled with a deeper understanding of the disease's pathophysiology, which facilitates the creation of more effective treatments.

Regional Insights

Geographically, North America held the largest market share in 2022, driven by a high prevalence of RVO-related risk factors, advanced healthcare infrastructure, and substantial healthcare expenditure. Europe followed closely, benefiting from similar factors and a growing elderly population. The Asia-Pacific region is projected to witness the fastest growth during the forecast period, fueled by increasing awareness of eye health, improving healthcare facilities, and a rising diabetic population, particularly in countries like China and India

Key Players

The RVO market features several prominent players dedicated to advancing treatment options and expanding their market presence. Notable companies include:

Regeneron Pharmaceuticals: Known for its innovative approach to ophthalmic diseases, Regeneron has been instrumental in developing effective therapies for RVO.

Novartis AG: A global healthcare leader, Novartis has invested significantly in research and development to address various retinal disorders, including RVO.

• Bayer AG: With a strong focus on eye care, Bayer has contributed to the advancement of treatments aimed at improving patient outcomes in RVO cases.

• Roche Holdings AG: Roche's commitment to ophthalmology has led to the development of cutting-edge therapies targeting retinal vein occlusion.

• Pfizer Inc.: As a major player in the pharmaceutical industry, Pfizer continues to explore novel treatment avenues for retinal diseases.

Conclusion

The Retinal Vein Occlusion market is on a trajectory of significant growth, driven by the increasing burden of vascular and ophthalmic disorders, technological advancements in treatment modalities, and strategic initiatives by key industry players. As the market evolves, stakeholders are poised to benefit from the expanding opportunities and innovations aimed at enhancing patient care and outcomes in RVO management.